Coal is the predominant energy source for power production in India, generating approximately 70% of total domestic electricity. Energy demand in India is expected to increase over the next 10-15 years; although new oil and gas plants are planned, coal is expected to remain the dominant fuel for power generation. Despite significant increases in total installed capacity during the last decade, the gap between electricity supply and demand continues to increase. The resulting shortfall has had a negative impact on industrial output and economic growth. However, to meet expected future demand, indigenous coal production will have to be greatly expanded. Production currently stands at around 290 Million tonnes per year, but coal demand is expected to more than double by 2010. Indian coal is typically of poor quality and as such requires to be beneficiated to improve the quality; Coal imports will also need to increase dramatically to satisfy industrial and power generation requirements.

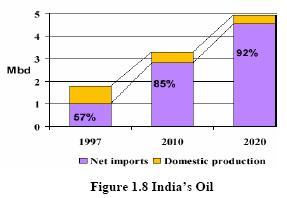

India's demand for petroleum products is likely to rise from 97.7 million tonnes in 2001- 02 to around 139.95 million tonnes in 2006-07, according to projections of the Tenth Five-Year Plan. The plan document puts compound annual growth rate (CAGR) at 3.6 % during the plan period. Domestic crude oil production is likely to rise marginally from 32.03 million tonnes in 2001-02 to 33.97 million tonnes by the end of the 10th plan period (2006-07). India’s self sufficiency in oil has consistently declined from 60% in the 50s to 30% currently. Same is expected to go down to 8% by 2020. As shown in the figure 1.8, around 92% of India’s total oil demand by 2020 has to be met by imports.

India's natural gas production is likely to rise from 86.56 million cmpd in 2002-03 to 103.08 million cmpd in 2006-07. It is mainly based on the strength of a more than doubling of production by private operators to 38.25 mm cmpd.

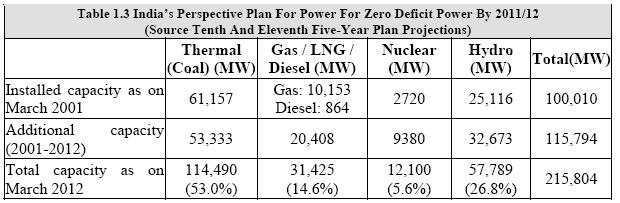

India currently has a peak demand shortage of around 14% and an energy deficit of 8.4%. Keeping this in view and to maintain a GDP (gross domestic product) growth of 8% to 10%, the Government of India has very prudently set a target of 215,804 MW power generation capacity by March 2012 from the level of 100,010 MW as on March 2001, that is a capacity addition of 115,794 MW in the next 11 years (Table 1.3).

In the area of nuclear power the objective is to achieve 20,000 MW of nuclear generation capacity by the year 2020.

Price of energy does not reflect true cost to society. The basic assumption underlying efficiency of market place does not hold in our economy, since energy prices are undervalued and energy wastages are not taken seriously. Pricing practices in India like many other developing countries are influenced by political, social and economic compulsions at the state and central level. More often than not, this has been the foundation for energy sector policies in India. The Indian energy sector offers many examples of cross subsidies e.g., diesel, LPG and kerosene being subsidised by petrol, petroleum products for industrial usage and industrial, and commercial consumers of electricity subsidising the agricultural and domestic consumers.

Grade wise basic price of coal at the pithead excluding statutory levies for run-of-mine (ROM) coal are fixed by Coal India Ltd from time to time. The pithead price of coal in India compares favourably with price of imported coal. In spite of this, industries still import coal due its higher calorific value and low ash content.

As part of the energy sector reforms, the government has attempted to bring prices for many of the petroleum products (naphtha, furnace oil, LSHS, LDO and bitumen) in line with international prices. The most important achievement has been the linking of diesel prices to international prices and a reduction in subsidy. However, LPG and kerosene, consumed mainly by domestic sectors, continue to be heavily subsidised. Subsidies and cross-subsidies have resulted in serious distortions in prices, as they do not reflect economic costs in many cases.

The government has been the sole authority for fixing the price of natural gas in the country. It has also been taking decisions on the allocation of gas to various competing consumers.

Electricity tariffs in India are structured in a relatively simple manner. While high tension consumers are charged based on both demand (kVA) and energy (kWh), the low-tension (LT) consumer pays only for the energy consumed (kWh) as per tariff system in most of the electricity boards. The price per kWh varies significantly across States as well as customer segments within a State. Tariffs in India have been modified to consider the time of usage and voltage level of supply. In addition to the base tariffs, some State Electricity Boards have additional recovery from customers in form of fuel surcharges, electricity duties and taxes.